Credit Builder Loans Explained: Are They Worth It?

If you’re trying to build or rebuild your credit, you may have heard about credit builder loans. Unlike traditional loans, they work a little differently designed specifically to help you establish positive payment history and boost your credit score.

But how do they work, and are they really worth it? Let’s break it down.

What Is a Credit Builder Loan?

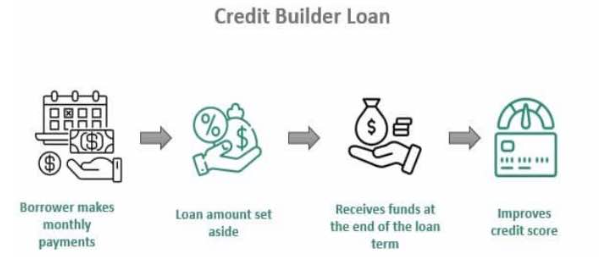

A credit builder loan is a type of installment loan aimed at people with no credit history or poor credit. Instead of receiving money upfront like a normal loan, the lender holds the loan amount in a secured savings account or certificate of deposit (CD).

-

You make monthly payments (usually $25–$100) over a set period, often 6–24 months.

-

Each payment is reported to the credit bureaus, helping you build a positive payment history.

-

At the end of the loan term, you get back the money you “borrowed” minus interest and fees.

Essentially, you’re borrowing from yourself while proving you can handle debt responsibly.

How Credit Builder Loans Help Your Credit

Credit scores are heavily influenced by two things:

-

Payment History (35% of your score) – Every on-time payment builds trust with lenders.

-

Credit Mix (10% of your score) – Having different types of credit (installment + revolving) is beneficial.

A credit builder loan improves both: it establishes a track record of on-time payments and diversifies your credit profile if you only have credit cards.

Pros of Credit Builder Loans

✅ Easier Approval – They’re designed for people with little to no credit, so requirements are flexible.

✅ Builds Payment History – Helps you establish the single most important factor in your credit score.

✅ Forces Savings – At the end of the term, you walk away with cash that can be used for an emergency fund.

✅ Low Monthly Cost – Payments are usually small and manageable.

Cons of Credit Builder Loans

❌ No Immediate Cash Access – You don’t get the loan funds until the end, so it won’t help in a financial emergency.

❌ Interest & Fees – You’ll pay to borrow your own money, which can make it feel less appealing.

❌ Takes Time – Building credit is not instant. It may take months before you see a noticeable improvement.

❌ Missed Payments Hurt – Late or missed payments will damage your score the opposite of your goal.

Who Should Consider a Credit Builder Loan?

A credit builder loan may be worth it if you:

-

Have no credit history and want to start building one.

-

Are recovering from past credit mistakes and need to show consistent positive payments.

-

Prefer a structured way to save money while improving your credit.

It may not be worth it if you already have good credit or if you urgently need funds.

Alternatives to Credit Builder Loans

-

Secured Credit Card – Requires a deposit but lets you build credit while using a credit card.

-

Authorized User Status – Piggyback on someone else’s good credit history.

-

Rent or Utility Reporting Services – Get everyday payments reported to the bureaus.

Final Thoughts: Are They Worth It?

Credit builder loans can be an excellent tool for people who are new to credit or looking to recover from past mistakes. While you won’t see overnight results, the steady progress can set you up for future financial success.

Think of it as a small investment in your credit future: pay on time, stick with the program, and you’ll walk away with both better credit and some savings in your pocket.