How to Build Credit from Scratch (Even with No History)

Everyone starts somewhere. If you’re just beginning your financial journey, you may face a common challenge: you have no credit history. Without it, lenders don’t know how trustworthy you are, which can make it tough to qualify for loans, credit cards, or even apartments.

The good news? You can build credit from scratch and it’s easier than you might think. With the right strategies, you can establish a strong foundation and set yourself up for long-term financial success.

Why Having No Credit Is a Problem

A “thin” credit file means you don’t have enough history for lenders to judge your financial behavior. Ironically, this can be as limiting as having bad credit. Without a score:

-

You may be denied loans or credit cards.

-

You’ll face higher deposits for rentals and utilities.

-

You won’t qualify for the best interest rates.

That’s why it’s important to start building credit as soon as possible.

Step 1: Open a Starter Credit Card

If you can’t qualify for a traditional credit card, consider:

-

Secured Credit Cards – You provide a deposit (often $200–$500), which becomes your credit limit. Use it responsibly, and it helps you build history.

-

Student Credit Cards – Designed for young adults with limited or no history.

👉 Tip: Use the card for small purchases and pay in full each month to avoid interest.

Step 2: Become an Authorized User

Ask a parent, sibling, or trusted friend with good credit to add you as an authorized user on their card. Their positive payment history can help boost your own credit file.

(Note: This works best if they have a long history of on-time payments and low balances.)

Step 3: Apply for a Credit-Builder Loan

Some banks and credit unions offer credit-builder loans, where you “borrow” a small amount that’s locked in a savings account. You make monthly payments, and once it’s paid off, you get the money—along with a positive credit history.

Step 4: Report Alternative Payments

Traditionally, rent and utility payments don’t appear on credit reports. But services like Experian Boost, Self, or rental reporting platforms let you add these payments to your credit history.

Step 5: Practice Smart Credit Habits Early

No matter which method you choose, the habits you build now will shape your financial future:

-

Pay on time, every time (payment history makes up 35% of your score).

-

Keep balances low (ideally under 30% of your available credit).

-

Avoid unnecessary applications—too many inquiries can hurt your score.

-

Check your credit reports regularly to track progress and catch errors.

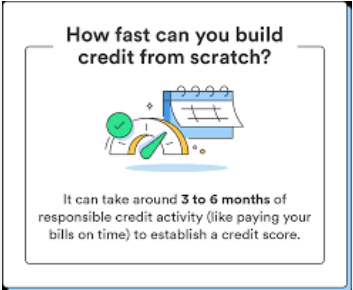

How Long Does It Take to Build Credit from Scratch?

You can usually get a credit score within 3 to 6 months of opening your first account. With consistent, responsible use, you can move from “no credit” to “good credit” surprisingly quickly.

Final Thoughts

Building credit from scratch may feel intimidating, but everyone starts with a blank slate. By using the right tools—like secured cards, credit-builder loans, and responsible spending—you can create a positive credit history and unlock future opportunities.