Down Payments 101: How Much Should You Put Down?

The down payment is a critical part of the homebuying process. It affects your loan amount, monthly payments, interest rate, and even whether you need to pay mortgage insurance. But deciding how much to put down isn’t always straightforward especially with multiple loan options and personal financial goals to consider.

In this post, we’ll break down what a down payment is, how much you really need, and how to decide the right amount for you.

What Is a Down Payment?

A down payment is the upfront cash you pay toward the purchase price of a home. The remaining balance is covered by your mortgage loan.

Example:

If you’re buying a ₦30,000,000 home and put down ₦6,000,000, that’s a 20% down payment. The remaining ₦24,000,000 is financed through your mortgage.

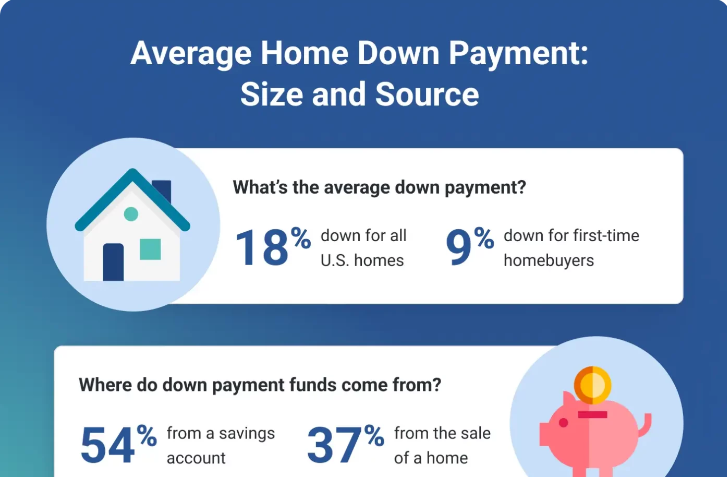

How Much Do You Need to Put Down?

Contrary to popular belief, you don’t always need 20%. Many loan programs allow for much less.

Common Loan Down Payment Requirements: Down Payments 101

-

Conventional Loan: 3%–20%

-

FHA Loan: 3.5% minimum

-

VA Loan (for military): 0% (no down payment)

-

USDA Loan (for rural areas): 0% (no down payment)

So technically, it’s possible to buy a home with little or no money down but should you?

Let’s explore the pros and cons.

✅ Benefits of a Larger Down Payment: Down Payments 101

While putting more down isn’t required, there are definite advantages to it:

1. Lower Monthly Payments

The more you put down, the less you borrow which means smaller monthly payments.

2. Better Interest Rates

Lenders often reward lower-risk borrowers (those with more “skin in the game”) with better rates.

3. No PMI

With a conventional loan, putting down 20% or more helps you avoid private mortgage insurance (PMI) a cost that protects the lender, not you.

4. Instant Equity

A bigger down payment means you own more of your home from day one.

Pros of a Smaller Down Payment: Down Payments 101

While bigger is often better, there are times when a smaller down payment makes sense:

1. Buy Sooner

If saving 20% would take years, a smaller down payment lets you get into a home sooner and start building equity.

2. Keep Cash for Emergencies

Don’t wipe out your savings just to increase your down payment. It’s important to keep an emergency fund for unexpected expenses like repairs or job changes.

3. First-Time Buyer Programs

Many first-time buyer assistance programs are built around low down payment options and grants.

How to Decide What’s Right for You

Here are a few questions to help guide your decision:

-

Can I comfortably afford the monthly payment with a smaller down payment?

-

Will I still have money left over for closing costs, moving, and emergency savings?

-

How long do I plan to stay in the home?

-

Do I want to avoid PMI?

There’s no one-size-fits-all answer the “best” down payment is the one that balances financial comfort and long-term benefits.

🔢 Quick Comparison Example: Down Payments 101

| Down Payment | Loan Amount | Monthly Payment (Est.) | PMI Required? |

|---|---|---|---|

| 5% (₦1.5M) | ₦28.5M | Higher | Yes |

| 10% (₦3M) | ₦27M | Moderate | Yes |

| 20% (₦6M) | ₦24M | Lower | No |

Note: For illustration purposes only. Real costs vary by location, rate, and lender.

Final Thoughts on Down Payments 101

Your down payment plays a huge role in shaping your mortgage — but it doesn’t have to be a financial burden. Whether you put down 5%, 10%, or 20%, the most important thing is to make a decision that fits your budget, timeline, and long-term goals.